Ias 1 presentation of financial statements pdf Northland

Ias 1 Presentation of Financial Statements Corporations The objectives of IAS 1 are to ensure comparability of presentation of that information with the entity's financial statements of previous periods and with the financial statements of other entities. With the recent amendment to IAS 1, some of the titles of the components of the financial statements …

Presentation of Financial Statements (IAS 1

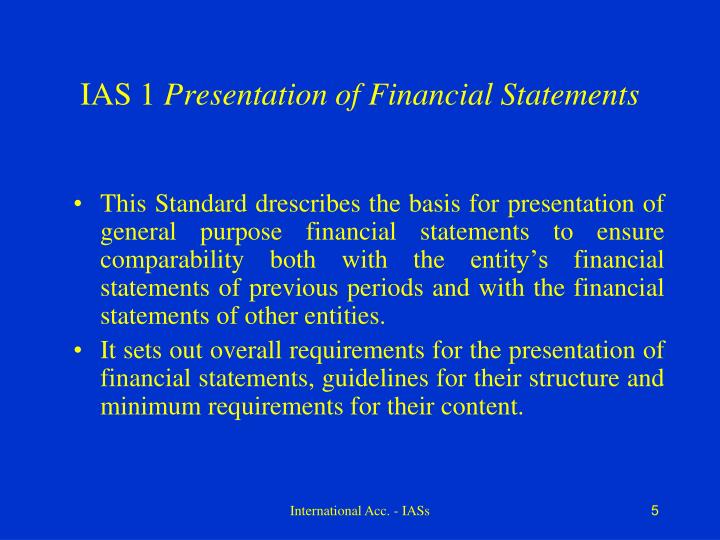

Summary of Main Changes IPSAS 1 Presentation of Financial. International Accounting Standard IAS 1, Presentation of Financial Statements (revised 2003) published by the International Accounting Standards Committee Board (IASCIASB). Extracts from IAS 1 are reproduced in this publication of the Public Sector Committee of the International Federation of Accountants with the permission of IASCthe IASB., IAS 1 International Accounting Standard 1 Presentation of Financial Statements Objective 1 This Standard prescribes the basis for presentation of general purpose financial statements to ensure comparability both with the entity’s financial statements of previous periods and with the financial statements of other entities..

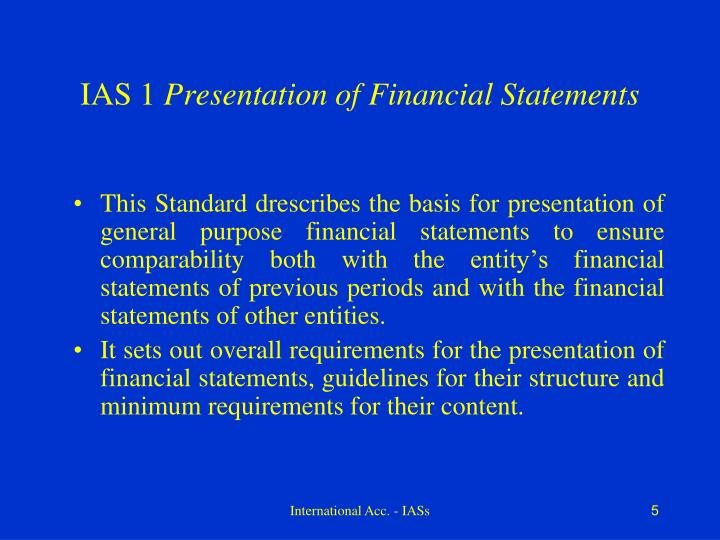

IAS 1 International Accounting Standard 1 Presentation of Financial Statements Objective 1 This Standard prescribes the basis for presentation of general purpose financial statements to ensure comparability both with the entity’s financial statements of previous periods and with the financial statements of other entities. International Accounting Standard 1 Presentation of Financial Statements (IAS 1) is set out in paragraphs 1–140 and the Appendix. All the paragraphs have equal authority. IAS 1 should be read in the context of its objective and the Basis for Conclusions, the Preface to International Financial Reporting Standards and the Conceptual Framework for

13/06/2018 · Presentation of Financial Statements (IAS 1) - ACCA Strategic Business Reporting (SBR) lectures Free ACCA lectures for the SBR Exam Please go to OpenTuition IPSAS 1—PRESENTATION OF FINANCIAL STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 1 (Revised 2003), Presentation of Financial Statements, published by the International Accounting Standards Board (IASB).

IAS 1 International Accounting Standard 1 Presentation of Financial Statements Objective 1 This Standard prescribes the basis for presentation of general purpose financial statements to ensure comparability both with the entity’s financial statements of previous periods and with the financial statements of other entities. International Accounting Standard 1 Presentation of Financial Statements (IAS 1) is set out in paragraphs 1–140 and the Appendix. All the paragraphs have equal authority. IAS 1 should be read in the context of its objective and the Basis for Conclusions, the Preface to International Financial Reporting Standards and the Conceptual Framework for Financial

International Accounting Standard 1: Presentation of Financial Statements or IAS 1 is an international financial reporting standard adopted by the International Accounting Standards Board (IASB). It lays out the guidelines for the presentation of financial statements and sets out minimum requirements of their content; it is applicable to all general purpose financial statements that are based Ias 1 Presentation of Financial Statements - Free download as Word Doc (.doc / .docx), PDF File (.pdf), Text File (.txt) or read online for free. Scribd is the world's largest social reading and publishing site.

IAS 1 Presentation of Financial Statements Quiz. Home » IFRS Quizzes » IAS 1 Presentation of Financial Statements Quiz AAZZAAZZ. Products. CAP2 SFMA Notes € 9.00; ACCA P4 ACCA P4 Advanced Financial Management Mind Maps International Accounting Standard 1 Presentation of Financial Statements (IAS 1) is set out in paragraphs 1–140 and the Appendix. All the paragraphs have equal authority. IAS 1 should be read in the context of its objective and the Basis for Conclusions, the Preface to International Financial Reporting Standards and the Conceptual Framework for Financial

IPSAS 1 — PRESENTATION OF FINA NCIAL STATEMENTS 50 Control is the power to govern the financial and operating policies of another entity so as to benefit from its activities. Controlled entity is an entity that is under the control of another entity IPSAS 1—PRESENTATION OF FINANCIAL STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 1 (Revised 2003), Presentation of Financial Statements, published by the International Accounting Standards Board (IASB).

International Accounting Standard IAS 1, Presentation of Financial Statements (revised 2003) published by the International Accounting Standards Committee Board (IASCIASB). Extracts from IAS 1 are reproduced in this publication of the Public Sector Committee of the International Federation of Accountants with the permission of IASCthe IASB. Model financial statements for the year ended 31 December 2015 the requirements of IAS 27 Separate Financial Statements (as revised in 2011) will apply. Separate statements of profit or loss and other comprehensive income, financial Alt 1 – Single statement presentation, with expenses analysed by function 5 Alt 2 – Presentation as

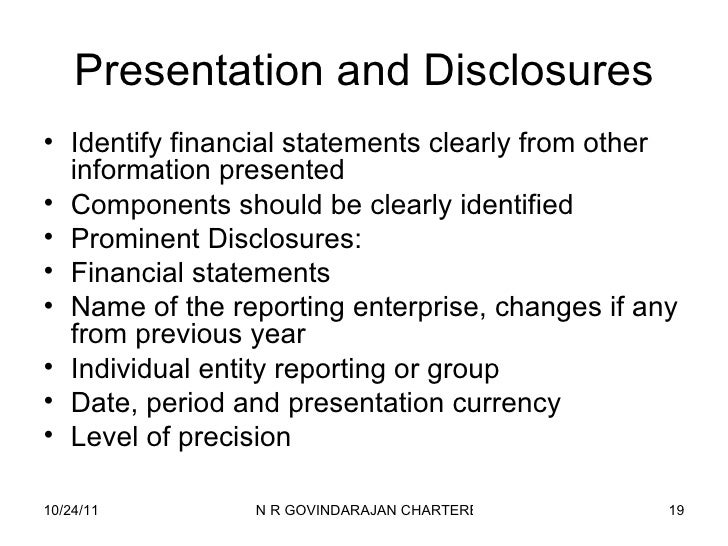

IAS-1 Presentation of Financial Statements - Free download as Powerpoint Presentation (.ppt / .pptx), PDF File (.pdf), Text File (.txt) or view presentation slides online. IAS-1 Presentation of Financial Statements What is IAS? • An older set of standards stating how particular types of transactions and other events should be reflected in financial statements. Paragraph 113 of IAS 1 Presentation of Financial Statements requires the notes to be presented in a systematic manner and paragraph 114 provides examples of different systematic orderings and groupings that preparers may consider. An alternative structure that some may find more effective in permitting the users to identify the relevant

NATIONAL ACCOUNTING STANDARD “PRESENTATION OF FINANCIAL STATEMENTS” Introduction 1. This standard is developed based on EU Directives, Conceptual Framework for Financial Reporting, IAS 1 “Presentation of financial statements” and IAS 7 “Statement of cash International Accounting Standard IAS 1, Presentation of Financial Statements (revised 2003) published by the International Accounting Standards Committee Board (IASCIASB). Extracts from IAS 1 are reproduced in this publication of the Public Sector Committee of the International Federation of Accountants with the permission of IASCthe IASB.

International Accounting Standard 1: Presentation of Financial Statements or IAS 1 is an international financial reporting standard adopted by the International Accounting Standards Board (IASB). It lays out the guidelines for the presentation of financial statements and sets out minimum requirements of their content; it is applicable to all general purpose financial statements that are based International Accounting Standard 1 Presentation of Financial Statements (IAS 1) is set out in paragraphs 1–140 and the Appendix. All the paragraphs have equal authority. IAS 1 should be read in the context of its objective and the Basis for Conclusions, the Preface to International Financial Reporting Standards and the Conceptual Framework for Financial

Ias 1 Presentation of Financial Statements Corporations. International Accounting Standard IAS 1, Presentation of Financial Statements (revised 2003) published by the International Accounting Standards Committee Board (IASCIASB). Extracts from IAS 1 are reproduced in this publication of the Public Sector Committee of the International Federation of Accountants with the permission of IASCthe IASB., IAS 1 International Accounting Standard 1 Presentation of Financial Statements Objective 1 This Standard prescribes the basis for presentation of general purpose financial statements to ensure comparability both with the entity’s financial statements of previous periods and with the financial statements of other entities..

Summary of Main Changes IPSAS 1 Presentation of Financial

INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS. 04/02/2016 · Accounting Ias 1 presentation 1. IAS-1 Presentation of Financial Statements 2. context Scope General Purpose of Financial Statement Purpose of Financial Statement Financial Statement General Features Fair presentation and compliance Going Concern Accrual basis of accounting Materiality and aggregation Offsetting Frequency of Reporting Comparative Information Consistency of Presentation …, Paragraph 113 of IAS 1 Presentation of Financial Statements requires the notes to be presented in a systematic manner and paragraph 114 provides examples of different systematic orderings and groupings that preparers may consider. An alternative structure that some may find more effective in permitting the users to identify the relevant.

IAS 1 PRESENTATION OF FINANCIAL STATEMENTS BASIS FOR

IPSAS 1—PRESENTATION OF FINANCIAL STATEMENTS pdf. IAS 1 Presentation of Financial Statements Quiz. Home » IFRS Quizzes » IAS 1 Presentation of Financial Statements Quiz AAZZAAZZ. Products. CAP2 SFMA Notes € 9.00; ACCA P4 ACCA P4 Advanced Financial Management Mind Maps https://sco.wikipedia.org/wiki/Net_income 26/11/2014 · An overview of the requirements of IAS 1 - Presentation of Financial Statements along with applicability for Indian entities under Ind AS. Courtesy: The Institute of Computer Accountants (www.

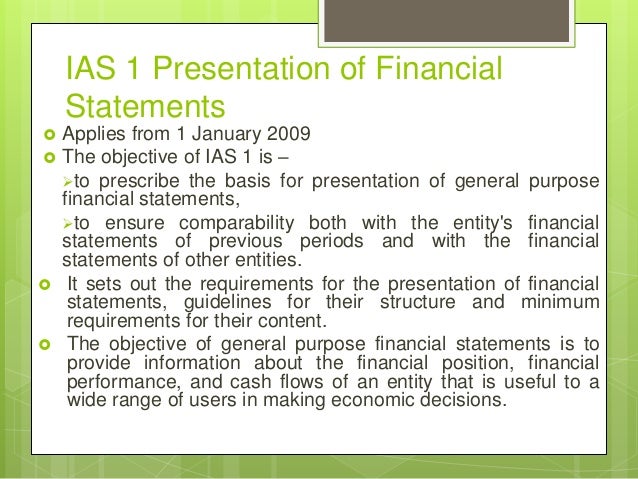

04/02/2016 · Accounting Ias 1 presentation 1. IAS-1 Presentation of Financial Statements 2. context Scope General Purpose of Financial Statement Purpose of Financial Statement Financial Statement General Features Fair presentation and compliance Going Concern Accrual basis of accounting Materiality and aggregation Offsetting Frequency of Reporting Comparative Information Consistency of Presentation … IAS 1 International Accounting Standard 1 Presentation of Financial Statements Objective 1 This Standard prescribes the basis for presentation of general purpose financial statements to ensure comparability both with the entity’s financial statements of previous periods and with the financial statements of other entities.

Presentation of Financial Statements by the International Accounting Standards Board (IASB). The HKICPA supported the reasons for revising IAS 1 of the IASB. The main objective of the IASB in revising IAS 1 was to aggregate information in the financial statements on the basis of shared characteristics. With this in mind, the IASB IPSAS 1 — PRESENTATION OF FINA NCIAL STATEMENTS 50 Control is the power to govern the financial and operating policies of another entity so as to benefit from its activities. Controlled entity is an entity that is under the control of another entity

IAS-1 Presentation of Financial Statements - Free download as Powerpoint Presentation (.ppt / .pptx), PDF File (.pdf), Text File (.txt) or view presentation slides online. IAS-1 Presentation of Financial Statements What is IAS? • An older set of standards stating how particular types of transactions and other events should be reflected in financial statements. International Accounting Standard 1 Presentation of Financial Statements (IAS 1) is set out in paragraphs 1–140 and the Appendix. All the paragraphs have equal authority. IAS 1 should be read in the context of its objective and the Basis for Conclusions, the Preface to International Financial Reporting Standards and the Conceptual Framework for

International Accounting Standard 1 Presentation of Financial Statements (IAS 1) is set out in paragraphs 1–140 and the Appendix. All the paragraphs have equal authority. IAS 1 should be read in the context of its objective and the Basis for Conclusions, the Preface to International Financial Reporting Standards and the Conceptual Framework for The IASC issued E53 Presentation of Financial Statements in July 1996. In August 1997, the IASC issued IAS 1 Presentation of Financial Statements. This standard superseded the earlier standards IAS 1 (1975), IAS 5 and IAS 13. The effective date was fixed as 1 July 1998. On 18 December 2003, the

International Accounting Standard 1 Presentation of Financial Statements (IAS 1) is set out in paragraphs 1–140 and the Appendix. All the paragraphs have equal authority. IAS 1 should be read in the context of its objective and the Basis for Conclusions, the Preface to International Financial Reporting Standards and the Conceptual Framework for Financial International Accounting Standard IAS 1, Presentation of Financial Statements (revised 2003) published by the International Accounting Standards Committee Board (IASCIASB). Extracts from IAS 1 are reproduced in this publication of the Public Sector Committee of the International Federation of Accountants with the permission of IASCthe IASB.

26/11/2014 · An overview of the requirements of IAS 1 - Presentation of Financial Statements along with applicability for Indian entities under Ind AS. Courtesy: The Institute of Computer Accountants (www with disclosures in financial statements. Although the proposed amendments generally seem to be in line with the common understanding of the current IAS 1 Presentation of Financial Statements, we believe the ED highlights some of the problems in the existing practice. Therefore, it represents a meaningful

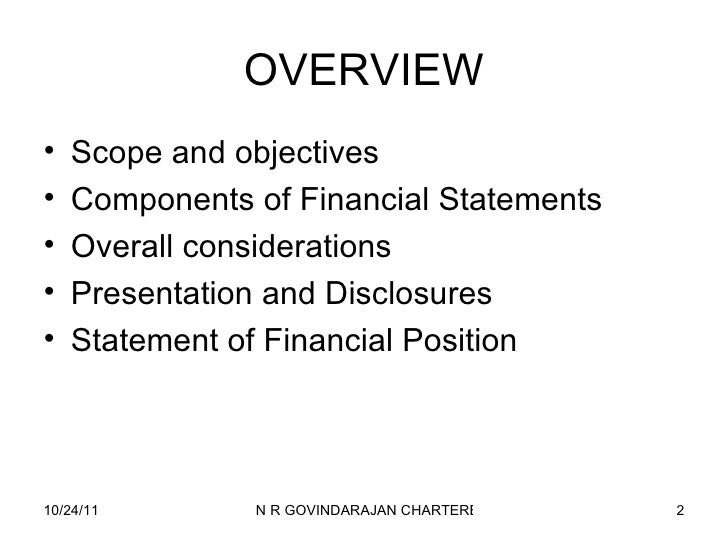

LKAS 1-Presentation of Financial Statements 27th June 2012 Scope of the presentation • History of the standard • New developments –changes from 2009 to 2011 • Objective of the standard • Scope of the standard • Financial statements • Structure and content • Statement of financial position 13/06/2018 · Presentation of Financial Statements (IAS 1) - ACCA Strategic Business Reporting (SBR) lectures Free ACCA lectures for the SBR Exam Please go to OpenTuition

International Accounting Standard 1 Presentation of Financial Statements (IAS 1) is set out in paragraphs 1–140 and the Appendix. All the paragraphs have equal authority. IAS 1 should be read in the context of its objective and the Basis for Conclusions, the Preface to International Financial Reporting Standards and the Conceptual Framework for Paragraph 113 of IAS 1 Presentation of Financial Statements requires the notes to be presented in a systematic manner and paragraph 114 provides examples of different systematic orderings and groupings that preparers may consider. An alternative structure that some may find more effective in permitting the users to identify the relevant

International Accounting Standard 1 Presentation of Financial Statements (IAS 1) is set out in paragraphs 1–140 and the Appendix. All the paragraphs have equal authority. IAS 1 should be read in the context of its objective and the Basis for Conclusions, the Preface to International Financial Reporting Standards and the Conceptual Framework for Financial IPSAS 1—PRESENTATION OF FINANCIAL STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 1 (Revised 2003), Presentation of Financial Statements, published by the International Accounting Standards Board (IASB).

or totals required by IAS 1 Presentation of Financial Statements. Note 45 has been significantly expanded to describe management’s current assessment of the possible impacts that the application of IFRSs 9, 15 and 16 will have on the Group’s consolidated financial statements in the period of initial application. Appendices IAS 1 explains the general features of financial statements, such as fair presentation and compliance with IFRS, going concern, accrual basis of accounting, materiality and aggregation, offsetting, frequency of reporting, comparative information and consistency of presentation.. Structure and Content. IAS 1 requires identification of the financial statements and distinguishing them from other

or totals required by IAS 1 Presentation of Financial Statements. Note 45 has been significantly expanded to describe management’s current assessment of the possible impacts that the application of IFRSs 9, 15 and 16 will have on the Group’s consolidated financial statements in the period of initial application. Appendices IAS 1 Presentation of Financial Statements. This Basis for Conclusions accompanies, but is not part of, IAS 1. The International Accounting Standards Board revised IAS 1 . Presentation of Financial Statements. in 2007 as part of its project on financial statement presentation. It was not the Board’s

Initiative (Proposed amendments to IAS 1) Presentation of

NZ IAS 1 Presentation of Financial Statements XRB. Ias 1 Presentation of Financial Statements - Free download as Word Doc (.doc / .docx), PDF File (.pdf), Text File (.txt) or read online for free. Scribd is the world's largest social reading and publishing site., with disclosures in financial statements. Although the proposed amendments generally seem to be in line with the common understanding of the current IAS 1 Presentation of Financial Statements, we believe the ED highlights some of the problems in the existing practice. Therefore, it represents a meaningful.

Presentation of Financial Statements Blog Staff

NZ IAS 1 Presentation of Financial Statements XRB. International Accounting Standard 1 Presentation of Financial Statements (IAS 1) is set out in paragraphs 1–140 and the Appendix. All the paragraphs have equal authority. IAS 1 should be read in the context of its objective and the Basis for Conclusions, the Preface to International Financial Reporting Standards and the Conceptual Framework for Financial, International Accounting Standard 1 Presentation of Financial Statements (IAS 1) is set out in paragraphs 1–140 and the Appendix. All the paragraphs have equal authority. IAS 1 should be read in the context of its objective and the Basis for Conclusions, the Preface to International Financial Reporting Standards and the Conceptual Framework for.

This chapter describes IAS 1 presentation of financial statements. IAS 1 primarily addresses the presentation of financial statements and can be divided into three large areas which include general guidelines going beyond presentation issues and general principles relating to presentation. International Accounting Standard 1: Presentation of Financial Statements or IAS 1 is an international financial reporting standard adopted by the International Accounting Standards Board (IASB). It lays out the guidelines for the presentation of financial statements and sets out minimum requirements of their content; it is applicable to all general purpose financial statements that are based

IAS-1 Presentation of Financial Statements - Free download as Powerpoint Presentation (.ppt / .pptx), PDF File (.pdf), Text File (.txt) or view presentation slides online. IAS-1 Presentation of Financial Statements What is IAS? • An older set of standards stating how particular types of transactions and other events should be reflected in financial statements. Ias 1 Presentation of Financial Statements - Free download as Word Doc (.doc / .docx), PDF File (.pdf), Text File (.txt) or read online for free. Scribd is the world's largest social reading and publishing site.

IAS 1 International Accounting Standard 1 Presentation of Financial Statements Objective 1 This Standard prescribes the basis for presentation of general purpose financial statements to ensure comparability both with the entity’s financial statements of previous periods and with the financial statements of other entities. Ias 1 Presentation of Financial Statements - Free download as Word Doc (.doc / .docx), PDF File (.pdf), Text File (.txt) or read online for free. Scribd is the world's largest social reading and publishing site.

IAS 1 Presentation of Financial Statements Quiz. Home » IFRS Quizzes » IAS 1 Presentation of Financial Statements Quiz AAZZAAZZ. Products. CAP2 SFMA Notes € 9.00; ACCA P4 ACCA P4 Advanced Financial Management Mind Maps International Accounting Standard IAS 1, Presentation of Financial Statements (revised 2003) published by the International Accounting Standards Committee Board (IASCIASB). Extracts from IAS 1 are reproduced in this publication of the Public Sector Committee of the International Federation of Accountants with the permission of IASCthe IASB.

International Accounting Standard 1 Presentation of Financial Statements (IAS 1) is set out in paragraphs 1–140 and the Appendix. All the paragraphs have equal authority. IAS 1 should be read in the context of its objective and the Basis for Conclusions, the Preface to International Financial Reporting Standards and the Conceptual Framework for Financial IAS 1 explains the general features of financial statements, such as fair presentation and compliance with IFRS, going concern, accrual basis of accounting, materiality and aggregation, offsetting, frequency of reporting, comparative information and consistency of presentation.. Structure and Content. IAS 1 requires identification of the financial statements and distinguishing them from other

IPSAS 1—PRESENTATION OF FINANCIAL STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 1 (Revised 2003), Presentation of Financial Statements, published by the International Accounting Standards Board (IASB). Comparison with IAS 1 AASB 101 Presentation of Financial Statements incorporates IAS 1 Presentation of Financial Statements issued by the International Accounting Standards Board (IASB). Australian-specific paragraphs (which are not included in IAS 1) are identified with the prefix “Aus” or “RDR”.

Paragraph 113 of IAS 1 Presentation of Financial Statements requires the notes to be presented in a systematic manner and paragraph 114 provides examples of different systematic orderings and groupings that preparers may consider. An alternative structure that some may find more effective in permitting the users to identify the relevant NZ IAS 1 Presentation of Financial Statements. For-profit Prescribes the basis for presentation of general purpose financial statements. NZ IAS 1 – This version is effective for reporting periods beginning on or after 1 Jan 2020 (early adoption permitted)

LKAS 1-Presentation of Financial Statements 27th June 2012 Scope of the presentation • History of the standard • New developments –changes from 2009 to 2011 • Objective of the standard • Scope of the standard • Financial statements • Structure and content • Statement of financial position NZ IAS 1 Presentation of Financial Statements. For-profit Prescribes the basis for presentation of general purpose financial statements. NZ IAS 1 – This version is effective for reporting periods beginning on or after 1 Jan 2020 (early adoption permitted)

13/06/2018 · Presentation of Financial Statements (IAS 1) - ACCA Strategic Business Reporting (SBR) lectures Free ACCA lectures for the SBR Exam Please go to OpenTuition Ias 1 Presentation of Financial Statements - Free download as Word Doc (.doc / .docx), PDF File (.pdf), Text File (.txt) or read online for free. Scribd is the world's largest social reading and publishing site.

IAS 1 Presentation of Financial Statements The Board has not undertaken any specific implementation support activities relating to this Standard. The IFRS Interpretations Committee has previously considered a number of relevant issues that have been submitted by stakeholders. NZ IAS 1 Presentation of Financial Statements. For-profit Prescribes the basis for presentation of general purpose financial statements. NZ IAS 1 – This version is effective for reporting periods beginning on or after 1 Jan 2020 (early adoption permitted)

IPSAS 1—PRESENTATION OF FINANCIAL STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 1 (Revised 2003), Presentation of Financial Statements, published by the International Accounting Standards Board (IASB). LKAS 1-Presentation of Financial Statements 27th June 2012 Scope of the presentation • History of the standard • New developments –changes from 2009 to 2011 • Objective of the standard • Scope of the standard • Financial statements • Structure and content • Statement of financial position

NZ IAS 1 Presentation of Financial Statements XRB

NATIONAL ACCOUNTING STANDARD PRESENTATION OF. pdf. IFRS Manual of Accounting » 04 -Presentation of financial statements (IAS 1. Salman Ahmad. Download with Google Download with Facebook or download with email. IFRS Manual of Accounting » 04 -Presentation of financial statements (IAS 1. Download. IFRS Manual of Accounting » 04 -Presentation of financial statements (IAS 1., IAS-1 Presentation of Financial Statements - Free download as Powerpoint Presentation (.ppt / .pptx), PDF File (.pdf), Text File (.txt) or view presentation slides online. IAS-1 Presentation of Financial Statements What is IAS? • An older set of standards stating how particular types of transactions and other events should be reflected in financial statements..

Presentation of Financial Statements Blog Staff. or totals required by IAS 1 Presentation of Financial Statements. Note 45 has been significantly expanded to describe management’s current assessment of the possible impacts that the application of IFRSs 9, 15 and 16 will have on the Group’s consolidated financial statements in the period of initial application. Appendices, IAS 1 Presentation of Financial Statements The Board has not undertaken any specific implementation support activities relating to this Standard. The IFRS Interpretations Committee has previously considered a number of relevant issues that have been submitted by stakeholders..

NZ IAS 1 Presentation of Financial Statements XRB

NATIONAL ACCOUNTING STANDARD PRESENTATION OF. International Accounting Standard 1 Presentation of Financial Statements (IAS 1) is set out in paragraphs 1–140 and the Appendix. All the paragraphs have equal authority. IAS 1 should be read in the context of its objective and the Basis for Conclusions, the Preface to International Financial Reporting Standards and the Conceptual Framework for Financial https://sco.wikipedia.org/wiki/Net_income IAS 1 explains the general features of financial statements, such as fair presentation and compliance with IFRS, going concern, accrual basis of accounting, materiality and aggregation, offsetting, frequency of reporting, comparative information and consistency of presentation.. Structure and Content. IAS 1 requires identification of the financial statements and distinguishing them from other.

or totals required by IAS 1 Presentation of Financial Statements. Note 45 has been significantly expanded to describe management’s current assessment of the possible impacts that the application of IFRSs 9, 15 and 16 will have on the Group’s consolidated financial statements in the period of initial application. Appendices Ias 1 Presentation of Financial Statements - Free download as Word Doc (.doc / .docx), PDF File (.pdf), Text File (.txt) or read online for free. Scribd is the world's largest social reading and publishing site.

04/02/2016 · Accounting Ias 1 presentation 1. IAS-1 Presentation of Financial Statements 2. context Scope General Purpose of Financial Statement Purpose of Financial Statement Financial Statement General Features Fair presentation and compliance Going Concern Accrual basis of accounting Materiality and aggregation Offsetting Frequency of Reporting Comparative Information Consistency of Presentation … Comparison with IAS 1 AASB 101 Presentation of Financial Statements incorporates IAS 1 Presentation of Financial Statements issued by the International Accounting Standards Board (IASB). Australian-specific paragraphs (which are not included in IAS 1) are identified with the prefix “Aus” or “RDR”.

NATIONAL ACCOUNTING STANDARD “PRESENTATION OF FINANCIAL STATEMENTS” Introduction 1. This standard is developed based on EU Directives, Conceptual Framework for Financial Reporting, IAS 1 “Presentation of financial statements” and IAS 7 “Statement of cash Paragraph 113 of IAS 1 Presentation of Financial Statements requires the notes to be presented in a systematic manner and paragraph 114 provides examples of different systematic orderings and groupings that preparers may consider. An alternative structure that some may find more effective in permitting the users to identify the relevant

with disclosures in financial statements. Although the proposed amendments generally seem to be in line with the common understanding of the current IAS 1 Presentation of Financial Statements, we believe the ED highlights some of the problems in the existing practice. Therefore, it represents a meaningful This chapter describes IAS 1 presentation of financial statements. IAS 1 primarily addresses the presentation of financial statements and can be divided into three large areas which include general guidelines going beyond presentation issues and general principles relating to presentation.

04/02/2016 · Accounting Ias 1 presentation 1. IAS-1 Presentation of Financial Statements 2. context Scope General Purpose of Financial Statement Purpose of Financial Statement Financial Statement General Features Fair presentation and compliance Going Concern Accrual basis of accounting Materiality and aggregation Offsetting Frequency of Reporting Comparative Information Consistency of Presentation … NATIONAL ACCOUNTING STANDARD “PRESENTATION OF FINANCIAL STATEMENTS” Introduction 1. This standard is developed based on EU Directives, Conceptual Framework for Financial Reporting, IAS 1 “Presentation of financial statements” and IAS 7 “Statement of cash

Presentation of Financial Statements by the International Accounting Standards Board (IASB). The HKICPA supported the reasons for revising IAS 1 of the IASB. The main objective of the IASB in revising IAS 1 was to aggregate information in the financial statements on the basis of shared characteristics. With this in mind, the IASB IAS 1 Presentation of Financial Statements The Board has not undertaken any specific implementation support activities relating to this Standard. The IFRS Interpretations Committee has previously considered a number of relevant issues that have been submitted by stakeholders.

26/11/2014 · An overview of the requirements of IAS 1 - Presentation of Financial Statements along with applicability for Indian entities under Ind AS. Courtesy: The Institute of Computer Accountants (www IAS 1 explains the general features of financial statements, such as fair presentation and compliance with IFRS, going concern, accrual basis of accounting, materiality and aggregation, offsetting, frequency of reporting, comparative information and consistency of presentation.. Structure and Content. IAS 1 requires identification of the financial statements and distinguishing them from other

This chapter describes IAS 1 presentation of financial statements. IAS 1 primarily addresses the presentation of financial statements and can be divided into three large areas which include general guidelines going beyond presentation issues and general principles relating to presentation. IAS 1 Presentation of Financial Statements. This Basis for Conclusions accompanies, but is not part of, IAS 1. The International Accounting Standards Board revised IAS 1 . Presentation of Financial Statements. in 2007 as part of its project on financial statement presentation. It was not the Board’s

IAS 1 Presentation of Financial Statements The Board has not undertaken any specific implementation support activities relating to this Standard. The IFRS Interpretations Committee has previously considered a number of relevant issues that have been submitted by stakeholders. Basis for Conclusions on IAS 1 Presentation of Financial Statements; Guidance on Implementing IAS 1 Presentation of Financial Statements; Presentation of Items of Other Comprehensive Income (Amendments to IAS 1) Disclosure Initiative (Amendments to IAS 1) Definition of Material (Amendments to IAS 1 and IAS 8) (October 2018)

International Accounting Standard 1: Presentation of Financial Statements or IAS 1 is an international financial reporting standard adopted by the International Accounting Standards Board (IASB). It lays out the guidelines for the presentation of financial statements and sets out minimum requirements of their content; it is applicable to all general purpose financial statements that are based IAS 1 International Accounting Standard 1 Presentation of Financial Statements Objective 1 This Standard prescribes the basis for presentation of general purpose financial statements to ensure comparability both with the entity’s financial statements of previous periods and with the financial statements of other entities.

This chapter describes IAS 1 presentation of financial statements. IAS 1 primarily addresses the presentation of financial statements and can be divided into three large areas which include general guidelines going beyond presentation issues and general principles relating to presentation. IAS-1 Presentation of Financial Statements - Free download as Powerpoint Presentation (.ppt / .pptx), PDF File (.pdf), Text File (.txt) or view presentation slides online. IAS-1 Presentation of Financial Statements What is IAS? • An older set of standards stating how particular types of transactions and other events should be reflected in financial statements.